Eminent Battle: A working-class community heads for a showdown

It’s a fight that pits a working class city ravaged by the housing crash against some of the most powerful players on Wall Street. The battle lines were drawn when the city of Richmond, California became the testing ground for using eminent domain—the law that allows governments to seize private property for the public good—to rescue “underwater” homeowners who owe more on their houses than they’re currently worth.

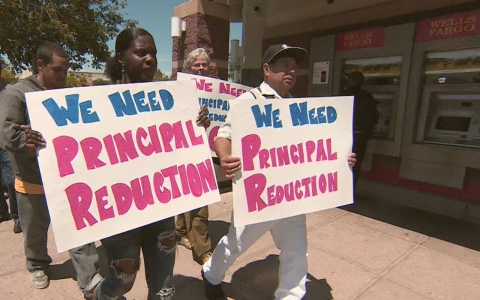

Using funds raised by a private advisory firm, Mortgage Resolution Partners (MRP), the city has offered to buy 624 troubled mortgages at current market values determined by a third party appraiser. The idea is to allow homeowners to refinance with cheaper loans, giving them equity in their houses and more money in their pockets to pump into the local economy.

The city called on the banks to sell the mortgages voluntarily by mid-August. The deadline passed with no takers. Now it’s up to the City Council to vote on September 10th whether to move forward with a plan to forcibly purchase the mortgages through eminent domain.

If Richmond votes yes, it will represent an unprecedented move for a city that has yet to reap the benefits of the housing recovery underway in other parts of the country. According to the latest figures from Zillow, 44 percent of Richmond homeowners are still underwater. Lower income, largely minority communities like Richmond, were prime targets for subprime lenders during the housing boom and the subsequent collapse in house prices devastated these communities through foreclosures, blight and shuttered businesses.

“We need our residents to have money in their pockets to frequent our local businesses,” Richmond Mayor, Gayle McLaughlin told Real Money. “This innovative program is a way to help the city as a whole, help the community, it has a public purpose and that’s really the definition of what eminent domain is all about.”

The financial industry disagrees. Several banks that administer mortgage-backed security trusts where the underwater loans reside are suing Richmond and its partner, MRP to block the plan. At the behest of big money managers including Pacific Investment Management Co and BlackRock Inc, Wells Fargo and Deutsche Bank were the first to take the city to court, arguing that Richmond and its advisors are attempting to profit at the expense of investors—a charge echoed by more than a dozen banking and financial services trade groups such as the Securities Industry and Financial Markets Association, The American Bankers Association, and the Investment Company Institute.

“The missing voice in this debate does seem to be the investor,” Investment Company Institute Chief Economist Brian Reid told Real Money. “We have nearly 55 million American families who are working and saving for retirement, we have another 24 million American families who have one or more retirees. They are all invested in mutual funds, in pension funds in exchange traded funds that own some of these securities that we’re talking about.”

The lawsuit claims the city’s offer prices aren’t fair and highlights the fact that 444 of the mortgages it’s attempting to buy are “performing” –meaning the homeowners are current on their payments. Such loans, the banks argue, are worth the full unpaid principal balance and “are not at serious risk of default,” nor are the homeowners “at risk of having their loans foreclosed and having to move out of their homes.”

But Steven Gluckstern, Executive Chairman of MRP which will take a $4500 flat fee for every loan restructured under the plan (the same fee banks can earn for restructuring mortgages under the government’s HAMP program) says that kind of reasoning is absurd. “Every defaulted loan was at some point performing,” he told Real Money. “All of the propensity or likelihood of a loan to default or not to default is embodied in the market value of that loan.”

The city and MRP contend the offer prices fairly reflect the greater risk premium associated with the type of mortgages they are seeking to purchase. None of the loans the city is targeting were safe enough to qualify for government guarantees. Instead, they’re locked in “private label securities”—loans that were pooled with other high risk loans and sold off in slices to a number of investors. Getting a majority of those investors to agree to write down an individual mortgage is next to impossible, meaning underwater homeowners with PLS loans have virtually no way of negotiating a principal reduction to lower their risk of default and foreclosure.

“The loans that ended up in these PLS trusts are the most toxic, the most likely to default, the worst,” said Gluckstern. “Think about it, they ended up there because they didn’t qualify for any of the federal guarantees or because the banks didn’t want to own them themselves, which they could have when they originated them.”

Gluckstern further contends that the legal process for eminent domain guarantees investors a fair deal. “The beauty about eminent domain is that there’s a process to determine value,” he said. “They have the right to argue any particular value they want and then a jury determines what the fair value is and then by definition they would have received the fair value.“

In addition to compensation, opponents of the plan also claim it fails to serve the public good because it could potentially choke off future mortgage lending to the city and harm the entire US mortgage industry if other communities follow Richmond’s lead.

“Fund managers have a legal obligation to put their investors first and when they do that they have to think about what would happen if I buy this type of bond or stock,” said ISI’s Brian Reid. “If they believe that a state or local government could come in and take this stock or bond in this case away from them, they’re going to be very reluctant to invest in this type of bond.”

Robert Hockett, a Cornell University Law Professor who dreamed up the idea of using eminent domain to buy PLS mortgages, says those fears are unfounded. “By far and away the hardest hit cities that are looking at plans like this are communities of color,” he told Real Money. “In effect the industry is saying we are going to deny credit to communities of color and that’s something that’s a threat that they know they can’t make good on because it would be violative of the nation’s fair lending laws. They would get into serious difficulty with the Department of Justice if they were to try that.”

Other cities including Newark, New Jersey and El Monte, California are also considering using eminent domain to help their struggling homeowners, while others have given similar plans the thumbs down including most recently, North Las Vegas.

As Richmond City Council prepares to vote Tuesday, the battle for Richmond’s hearts and minds rages online through social media and websites Richmond Cares which aims to galvanize support for the plan—and the opposition’s counterpunch, Stop Investor Greed.

Error

Sorry, your comment was not saved due to a technical problem. Please try again later or using a different browser.