Economy

With the possible passage of a "mini" grand bargain to resolve the D.C. deadlock, political leaders on both sides of the aisle will be kicking the can down the road.

Limited success for a Senate compromise bill would address twin federal woes: A government shutdown since Oct. 1 due to congressional inability to pass a budget for the 2014 fiscal year and a rapidly approaching Oct. 17 loose deadline for the debt ceiling.

The agreed-upon bipartisan deal could extend the Treasury's borrowing authority until February, thereby setting a new cap above $17 trillion. It would also re-open the government and send furloughed employees back to work through the beginning of next year.

Republicans are poised to gain a delay in the start of the employer reinsurance tax included in the Affordable Care Act, while Democrats aim for more flexible and reduced sequester cuts — all part of a long-term plan that could take shape by December.

But without such an agreement, the Treasury says the country could face catastrophic results: "Credit markets could freeze, the value of the dollar could plummet, U.S. interest rates could skyrocket, the negative spillovers could reverberate around the world."

Al Jazeera looks at some of the questions at the heart of ongoing fiscal uncertainty:

Has the U.S. ever defaulted on its debt?

Contrary to statements by politicians and financial leaders, the Treasury has indeed failed to meet its obligations before.

In 1814 and 1979, there were two relatively contained examples of U.S. default on sovereign debt.

The first was during the War of 1812, when the capital was on fire and U.S. troops were fighting unpaid. The second occurred at the end of the turbulent 1970’s, when a bureaucratic glitch prevented the federal government from paying $122 million in Treasury bills, costing taxpayers billions.

Bond markets panicked at the “delay” in payments, which investors unambiguously labeled a “default.” There were two additional debatable defaults involving late 18th century war debts and the transition from the gold standard in 1933.

The financial disaster predicted by economic analysts for the coming weeks could dwarf the prior default episodes — and the near-default shock of 2011, after which the U.S. credit rating was downgraded and the market tanked.

How much will the U.S. owe by Oct. 17?

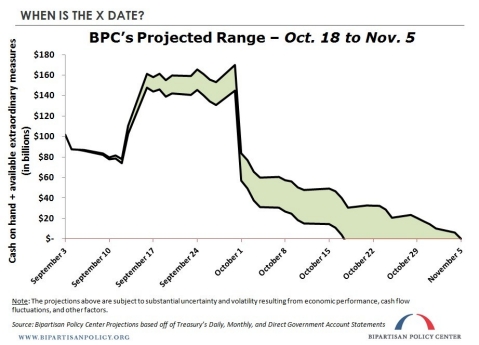

Beyond the approximate Oct. 17 date of earliest possible default, the Treasury is thought to be able to cover its obligations for another two weeks.

The Treasury already hit the debt limit in May, reaching the $16.699 trillion cap that Congress had placed on national borrowing in January.

However, through $412 billion worth of “extraordinary measures,” the government has been able to pay its bills and interest payments on an IOU that now exceeds $52,880 per citizen.

As of Monday, the Treasury said total public debt had reached $16.747 trillion. Other tallies place the exact amount, essentially frozen for the past five months, at $16.755 trillion.

Some analysts say Nov. 1 — when the government must pay out $58 billion in benefits — is the real "doomsday." The Bipartisan Policy Center suggests the government could fall $106 billion short by Nov. 15.

U.S. bonds thrive on being the most reliable investment in the world, but this could change once the Treasury has just $30 billion in cash on hand.

At any rate, the debt ceiling will need to increase to an estimated $25 trillion by 2023.

Can the president decide whom to pay in a default?

Some Republicans in the tea party caucus reject the fact that the U.S. could legitimately default on its debt. Others accept the idea of default but downplay the impact. Taking a third stance, Ted Yoho, R-Fla., has said the event would actually stabilize world markets.

Many debt-ceiling deniers argue that the government can prioritize its payments after the “artificial” deadline on Thursday by simply paying off foreign and domestic creditors but not pensioners.

"There's always revenue coming into the Treasury, certainly enough revenue to pay interest," Rep. Justin Amash, R-Mich, told the National Journal. "Democrats have a different definition of 'default' than what we understand it to be. What I hear from them is, 'If you're not paying everything on time, that's a default.' And that's not the traditionally understood definition."

Representatives like Amash say the Treasury could continue to process vital Fedwire payments but not pay Medicare reimbursements, for example. As the federal government has done with its employees during the shutdown, they advocate meeting essential obligations while postponing non-essential bills.

This logic may sound plausible but does not reflect how the process works, Democrats argue.

The Treasury’s official stance is the following: the government cannot legally decide to pay certain bills and ignore others; the system does not have the technical capacity to rank payment importance; the volume of funds varies significantly from day to day; and just paying bondholders would fail to resolve the core issue.

Is deficit reduction the real political issue?

The good news this year is that the budget deficit is only 4 percent of gross domestic product (GDP), down from a high of 10 percent after the financial crisis in 2009.

The 2013 deficit -- the amount that annual U.S. government revenues fall short of outlays -- totals around $700 billion, since taxes came in higher than expected.

Thus, the public debt ordinarily would have jumped by that amount, as the country borrowed to finance fresh expenditures.

Under current sequestration law, the deficit is expected to continue shrinking through 2015.

However, deficits are then set to rise again, which the Congressional Budget Office (CBO) attributes to “the pressures of an aging population, rising health care costs, an expansion of federal subsidies for health insurance and growing interest payments on federal debt.”

Defenders of President Barack Obama’s economic record attribute high recent deficits to a recession worse than any since the Depression.

After bailing out failed banks and undertaking a massive stimulus effort, the deficit climbed to historic levels unseen since the aftermath of World War Two. This came on the heels of huge wartime spending under George W. Bush.

Will the U.S. budget ever return to the black?

The late 1990’s saw a surplus, following a balanced budget and sustained prosperity.

Today there is fundamental disagreement about how to pay for the future and a genuine lack of consensus about national priorities. "Obamacare," the main bone of the shutdown showdown between Democrats and Republicans, is just one of several key items. The dispute also focuses on tax rates, discretionary spending and mandatory programs.

Joshua Gordon, policy director at the non-partisan Concord Coalition, says that a “pragmatic” approach is best.

“But this may not be the best word because it doesn’t work so well right now,” Gordon says. “You assume that both sides need to give something in order to complete negotiations.”

Many Republicans argue that the growth of Social Security and Medicare should be curtailed to shore up the long-term fiscal health. While most Democrats would not back aggressive attempts to dismantle the safety net, the Obama administration hopes to address ballooning entitlement and interest costs.

At around 30 percent of the federal budget, discretionary federal spending (i.e. on the military, education and the environment) is headed toward the lowest share of GDP in more than 70 years. But many legislators from both parties are uncomfortable with the severity of cuts for the Defense Department.

A CBO report last month predicted that by 2038 medical costs would skyrocket from 4.6 percent to 8 percent of GDP. In the same 25-year period, the number of people projected to receive Social Security benefits would nearly double to 100 million. And the debt is slated to reach 100 percent of GDP by then, with the deficit at 6.5 percent of GDP.

The debt-to-GDP ratio was at 36 percent in 2007 but has more than doubled to 76 percent for 2014.

The political debate hinges on whether the government should implement more cuts now or resort to much steeper cuts later on.

After President Obama’s perceived January victory in implementing tax increases for higher earners, Republicans are loathe to back the Democrats’ preference for rate hikes and minor entitlement cuts. Instead, they seek much more drastic reduction in long-term entitlement spending.

Due to the sequester, the deficit (and thus the national debt problem) will improve for the next half-decade, assuming that Congress, the political body vested with the Constitutional power to increase the debt ceiling, fulfills its duty. But any surplus is highly unlikely for now.

If the economy grows, is big national debt a problem?

For starters, the U.S. benefits from being able to print the currency that the rest of the world needs. Therefore, it doesn’t play by the same debt rules as other nations.

The real debt issues are forecast to return by 2020, as interest rates rise to normal levels. More federal borrowing will crowd out savings and put downward pressure on wages -- even as productivity gains are expected to continue.

In addition, high debt burden decreases investor confidence and makes it more difficult for lawmakers to respond flexibly in times of trouble.

In the long run, a debt that grows faster than GDP is unsustainable. In support of more frugal tax-and-spending policies, the CBO has called for “letting revenues rise more than they would under current law, reducing spending for large benefit programs below the projected levels, or adopting some combination of those approaches.”

Hard choices are arguably required beyond the reach of the current sequester, but politicians fear an economic tradeoff.

Waiting to confront the problem will create more debt on which to pay interest at higher rates. But making more painful budget decisions sooner will enfeeble the economic recovery and most likely result in negative short-term impact on GDP and employment.

Keynesians such as columnist Paul Krugman argue that fiscal policy makers should focus on promoting growth. Analysts Robert Pollin and Michael Ash suggest there is minimal risk of drop-off in output even as public debt approaches the value of GDP.

“History suggests that there is some threshold beyond which piling on public debt definitively yields lower economic growth,” Pollin and Ash say. “But there is no consensus on what that threshold is, and the evidence suggests, in any event, that the United States and Europe are not anywhere close to it.”

On the other side of the debate are “Austerians” such as economists Carmen Reinhart and Kenneth Rogoff, who say deficit reduction and paying down the debt are the best way to guarantee economic success.

If lawmakers took the advice of experts, the debt ceiling could be eliminated and the president would never again be forced to consider minting two $1 trillion platinum coins.

Error

Sorry, your comment was not saved due to a technical problem. Please try again later or using a different browser.