Ali Velshi On TargetMon-Fri 9pm ET/6pm PT

Lucas Schifres / Getty Images

On Aug. 11, a few minutes before the close of stock trading in China, its central bank made its biggest one-day intervention and lowered the value of its currency, the yuan, by 1.9 percent. The yuan, pegged against the U.S. dollar, is allowed to vary in value only within a fixed band. Global investors, caught off guard, struggled to understand the motive behind the move, and international free-trade critics seized the opportunity to increase calls for stricter rules regarding currency manipulation in ongoing free-trade deal negotiations.

But much of the debate on both counts lacks complete context.

“We believe the primary motivation was to better align their foreign exchange regime to IMF guidance,” Beata Caranci, the chief economist at TD Bank, wrote in a note after the devaluation. China’s ambitions include an inclusion in the International Monterey Fund’s (IMF) pool of global reserve currencies, a key requirement for which is a yuan more closely aligned with market rates. Before the Chinese central bank acted Bloomberg data shows a sustained difference between the markets pricing of the yuan, which was about 2 percent lower than the fixed peg.

Following the move, the IMF hinted at a possible inclusion of the yuan in the global reserve currency basket by extending the effective date for any future change to “allow users sufficient lead time to adjust in the event that a decision were to be taken to add a new currency.” A decision on the yuan is expected in November .

But critics are quick to label the Chinese central bank’s move currency manipulation aimed at making Chinese exports cheaper. This argument runs the risk of misinformation.

China’s currency has appreciated 30 percent since the country ended its fixed rate in 2005. In other words, the price of Chinese exports to the U.S. has risen by one-third. The inflation-adjusted price of global Chinese exports has gone up almost 40 percent over the last two years, according to research by Michael W. Klein, an international economic affairs professor at Tufts University. At the same time, the Chinese government has opened up regulated access to its capital markets through its qualified foreign institutional investor programs.

To be sure, concerns around China are real. While there’s little debate about the dissatisfaction with China’s nontransparent economic policies, largely restricted access to capital markets and managed-peg currency pricing, the jury is still out on whether it is a currency manipulator.

The key issue is what constitutes currency manipulation. Free-trade-deal critics largely define it as foreign governments’ purchasing large quantities of U.S. debt, which boosts the value of the dollar and suppresses the value of their currencies. This makes their exports relatively cheaper and pressures U.S. manufacturers to move their operations to less expensive venues abroad. James P. Hoffa, the general president of the International Brotherhood of the Teamsters, calls the issue “a cancer for trade deals.”

That’s why calls to oppose the Trans-Pacific Partnership, a free-trade agreement being negotiated among 12 nations around the Pacific Rim, have grown louder since the devaluation. China is not among the participating countries but could join the agreement in the future.

The U.S. Treasury Department has labeled only three countries as currency manipulators: Japan in 1988, Taiwan in 1988 and 1992 and China from 1992 through 1994. The Treasury has not deemed China or any other country a manipulator since. In 1994 the U.S. joined the World Trade Organization (WTO), thereby agreeing to resolve all trade disputes, including any currency manipulation disputes, through the WTO and giving up the right to unilateral action.

The WTO defers to the International Monetary Fund (IMF) to assess whether a country manipulates its currency to gain unfair advantage, which is prohibited by both agencies. The IMF has no criteria for designating a country a currency manipulator and has never done so for any of its 188 member nations. The Wall Street Journal quotes the IMF’s legal department as saying its ban on currency manipulation “is a relatively complex provision, and not all of its terms are easily understood or easily applied.”

Without consensus on the issue of currency manipulation, debate abounds.

The United States is the single biggest source of funds for the IMF. Congress has questioned funding for the IMF, which the Treasury Department defended for its criticality in maintaining U.S. commercial interests in international negotiations.

Even so, the IMF and the U.S. are at odds over the current state of China’s currency. In an April 2015 report, the IMF noted the yuan is fairly valued, while the Treasury Department’s report to Congress called it undervalued.

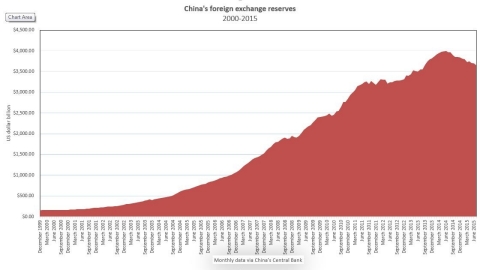

Part of the U.S. discontent stems from China’s growing dollar reserves, which drive up the value of the dollar and hold down the value of the yuan. As of March 2015, China’s foreign exchange reserves were $3.73 trillion, or 40 percent of its GDP.

But many critics ignore other countries such as Switzerland, which has foreign currency reserves of 73 percent of its GDP, according to the Congressional Research Service. Low in absolute terms, it is substantial relative to the size of its economy and is enough to give Swiss exports an unfair advantage while much of the eurozone struggles.

On the other side of the spectrum are emerging economies that accuse the United States’ and the United Kingdom’s central banks and the European Central Bank of maintaining monetary policies — such as quantitative easing, or creating money to buy assets, thus increasing private-sector spending — that stoke inflation and cause bubbles in emerging market assets.

The Congress Research Service’s latest report on currency manipulation highlights Brazil’s argument that quantitative easing in developed countries was a key factor in causing its currency, the real, to appreciate by more than 25 percent against the dollar from the start of 2009 through the end of the third quarter of 2010. Brazil’s finance minister declared that a currency war had broken out in the global economy, and the country imposed short-term controls on flows of capital into Brazil to reduce the real’s rise.

Combined, more than 20 countries have increased their foreign exchange reserves by nearly $1 trillion annually for several years by intervening in foreign currency markets, according to a December 2012 study by economists at the Peterson Institute of International Economics. The study identifies China, Denmark, Hong Kong, South Korea, Malaysia, Singapore, Switzerland and Taiwan as most heavily engaged in currency interventions.

While it may be decades before any debates on currency manipulation are settled, the immediate question relates to congressional approval of the Trans Pacific Partnership.

From a geopolitical standpoint, foreign policy strategists see the trade deal as a way for the U.S. to reach out to China’s neighbors, wary of Beijing’s rapidly growing influence, without including China in the discussions. By pressing ahead, Washington may gain an important lever in ongoing negotiations about free markets with Beijing.

Error

Sorry, your comment was not saved due to a technical problem. Please try again later or using a different browser.